Assess the view that a rise in Ireland's corporation tax rate is likely to have a damaging effect on its macroeconomic performance

AQA A-Level Economics Paper 2 June 2023 Insert

Assess the view that a rise in Ireland's corporation tax rate is likely to have a damaging effect on its macroeconomic performance. (25 marks)

- Paragraph 1

- Argument: on the one hand, higher corporation tax rates are damaging as they can reduce long-term economic growth

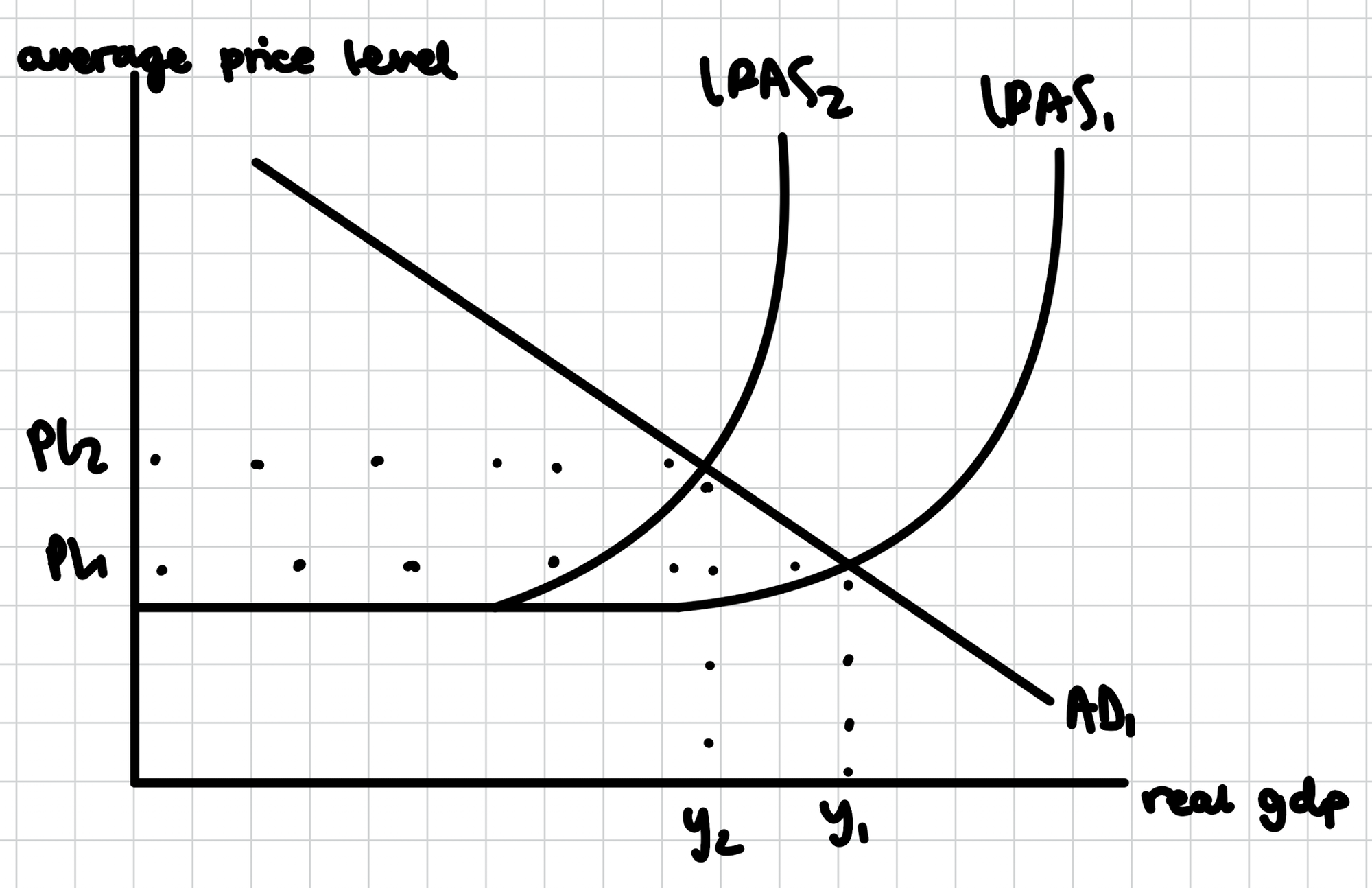

- Diagram: LRAS shifting left

- Evaluation: depends on the time lag + size of the tax

- Paragraph 2

- Argument: on the other hand, higher corporation tax rates are not damaging as higher tax revenue can enable more spending

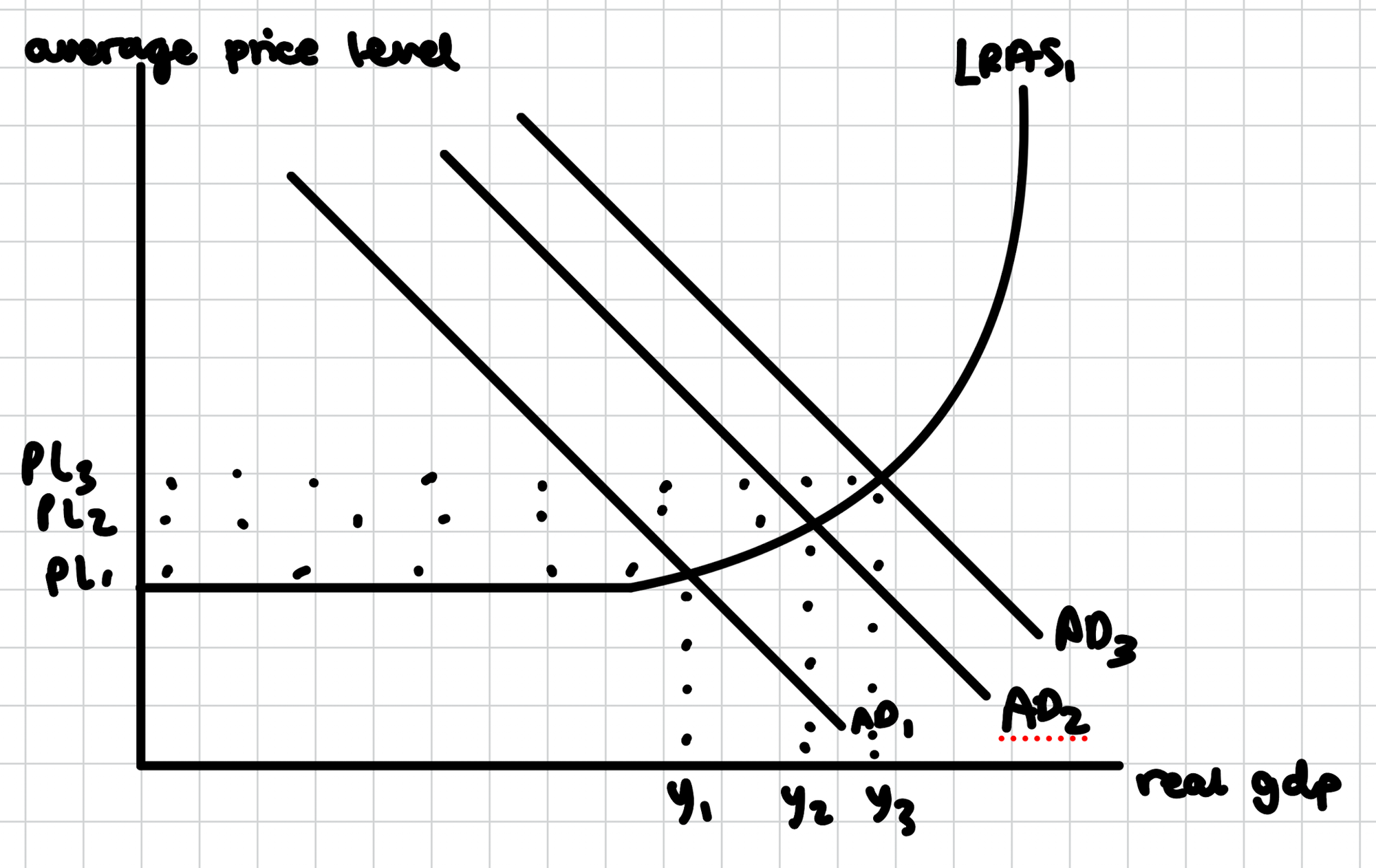

- Diagram: AD shifting right, multiplier effect

- Evaluation: less business confidence and less investment

Higher corporation taxes in Ireland are likely to impact macroeconomic performance as there this would have an impact on economic growth, unemployment and inflation in Ireland's economy. Higher corporation taxes can be seen as a form of contractionary fiscal policy, but they can also have an effect on the supply side of Ireland's economy.

On the one hand, an increase in Ireland's corporation tax is likely to be damaging to their macroeconomic performance as it would cause their trend rate of economic growth to fall. Higher corporation taxes reduce the incentive for firms to set up in Ireland's economy. The extract mentions that Ireland were previously able to attract MNCs like TikTok and Apple to set up in the country as they were incentivised by the higher levels of profit that they could retain. So, not only would firms consider exiting, but they would also have less profit left to reinvest into capital and machinery, which causes productivity to fall. Due to this, the productive potential of the economy decreases and the effect of this can be seen by the diagram below, which shows a decrease in LRAS from LRAS1 to LRAS2, leading to a decrease in economic growth from Y1 to Y2. A slower rate of trend rate of economic growth can increase inflation in the economy as it pushes the economy into a positive output gap.

However, a decrease in long-run aggregate supply may not be so damaging for two main reasons. Firstly, depending on the state of the economy, a decrease in LRAS may have little effect on output or inflation, particularly if the economy was already experiencing a negative output gap and had spare capacity. Secondly, it is possible that Ireland has implemented supply-side policies other than lower corporation taxes, which can offset the effect of higher corporation taxes. For example, low income taxes can incentivise workers to work harder to achieve promotions, which offsets the impact of firms reducing their spending on capital goods.

On the other hand, an increase in Ireland's corporation tax rate can have a positive impact on their macroeconomic performance, as higher corporation taxes can lead to an increase in tax revenue. Extract C mentions that it could lead to an extra €12.4 billion in corporation tax revenue, which can fund government spending. The extract mentions government spending can be increased on pensions and social care. As the government increases spending on pensions, disposable incomes among the elderly rise. As incomes rise, consumer spending increases. Since consumer spending is a component of aggregate demand, aggregate demand also increases. As aggregate demand shifts to the right, this leads to higher economic growth, as shown by the diagram below. This could also produce a positive multiplier effect. As consumers spend more at local coffee shops, bars, and restaurants, staff earn higher incomes and businesses see more revenue. This can lead to further increases in both consumer and business spending, boosting aggregate demand even more. Overall, higher corporation taxes increase government spending, which stimulates further growth compared with a scenario where corporation taxes are lower.

However, the overall effect of demand-side policies such as spending on welfare depends on the size of the multiplier. The multiplier is given by the equation 1/(1 − marginal propensity to consume). In this case, if the government chose to increase spending on pension, this might lead to a larger multiplier effect as pensioners have low income due to retirement. Depending on the size of the multiplier, the economy could experience different levels of inflation as it approaches its capacity.

Overall, my view is that higher corporation taxes would not be damaging to Ireland’s economy. The higher tax revenue can be used to boost spending and growth, whilst the main downsides are arguably negligible. The potential hit to the supply-side would be minimal since the proposed increase in corporation tax rates would likely be too small to incentivise MNCs would relocate, since Ireland would still offer a tax rate similar to many other European countries.

A-Level Economics Tutoring

I offer one-to-one and small group A-Level Economics tutoring for students across the UK and internationally. With 87+ five-star Google reviews and tutoring experience since 2017, I specialise in helping students understand difficult concepts and improve their exam technique.